Calculating GST & WHT on OTA commissions

by Madeeh Ahmed, Tax Advisor

Note: Rules on the imposition of WHT on OTA commission have been changed via the amendments brought to the BPT Regulation after this blog post was published. We advise you not to rely simply on the information provided here but to seek professional assistance, especially with respect to the changes to the application of WHT. We will soon update the post to reflect the recent developments.

If you conduct a tourism sector business, it is highly likely that you deal with Online Travel Agents (“OTA”) on a regular basis. In the past, accounting for tax (especially Withholding Tax and Goods and Services Tax) in relation to OTA commission has been rather simple and straightforward. However, there have recently been some changes to the tax treatment of OTA commissions and I understand that many are having difficulty in dealing with those changes.

Before going into what the changes are and how they may impact you, let me shortly sum up the main business models used by OTAs working with hotels in the Maldives:

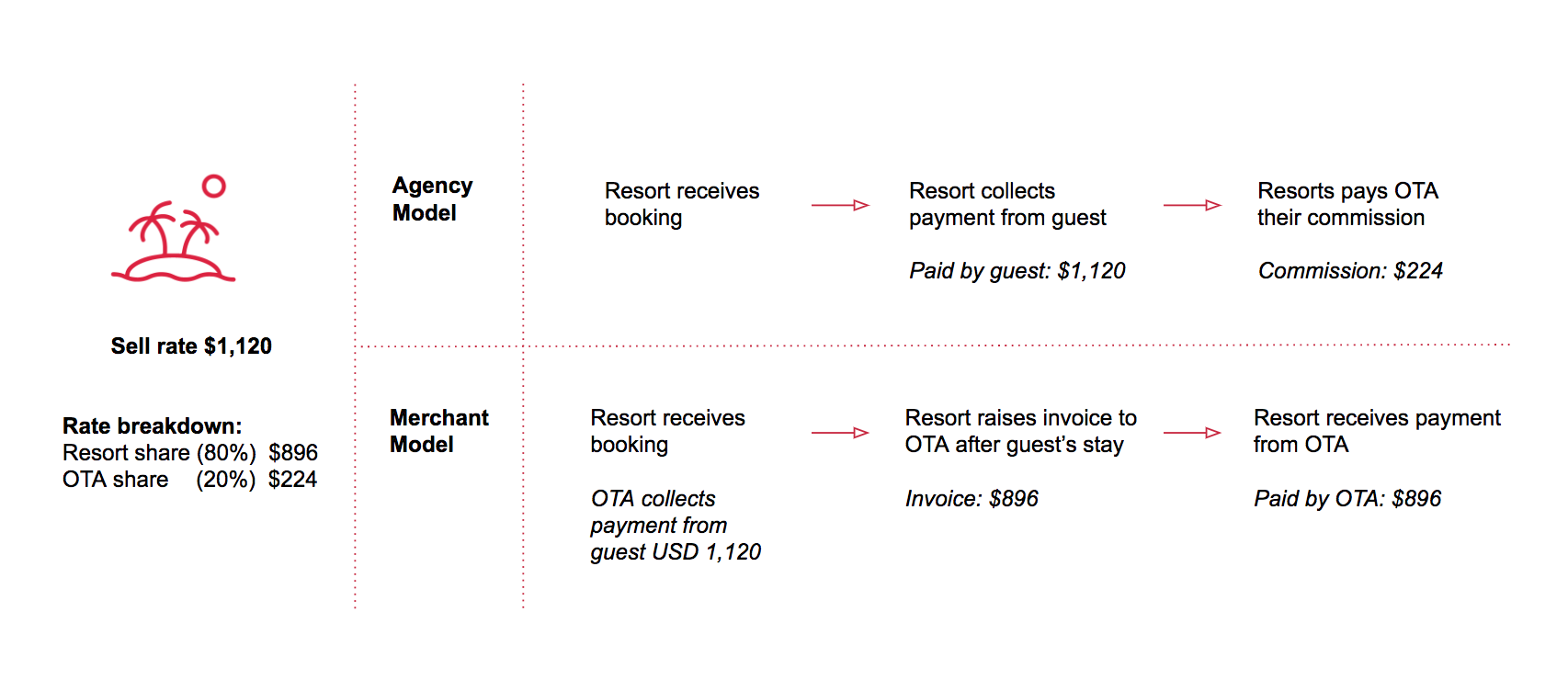

1. Agency Model

Under this model, hotels normally collect payments from the guests and OTAs receive a commission on bookings made via their websites.

Accounting for tax is simple under this model since the hotel raises invoices to guests at the ‘Sell Rate’ offered in the OTA’s website, GST is calculated based on this amount (understandably, you will have to make adjustments for Green Tax and such deductions).

As far as WHT is concerned, you receive an invoice (for the commission amount) from the non-resident OTA, and calculation of WHT on this amount is simple.

2. Merchant Model

Under this model, the OTAs normally collect payment from guests at the time of booking confirmation. The hotel will be entitled to an amount equal to the room rate minus compensation/commission charged by the OTA. Following the guest check out (or any other time as agreed with the OTA), the OTA will remit the ‘Net Amount’ of revenue (after deducting the OTAs commission) to your account, and you may raise an invoice to the OTA with the net amount of revenue you are entitled to.

In my experience, many tourism businesses have, in the past, not declared WHT on this transaction, because there was no ‘obvious’ commission payment from the hotel to the non-resident OTA. Under this arrangement, unlike the agency model, you do not receive an invoice from the OTA that specifies any commission amount.

Likewise, your GST on this transaction is based on the Net Amount charged from OTA, because this is the amount for which you issue a tax invoice and hence, that is what is reflected in your management reports.

In this article, my main focus is the second model which has recently caused trouble with many hotels and resorts in the tourism sector.

For the sake of brevity, the differences between the two models I’ve mentioned above, are illustrated below:

So what changed?

In the past, there has not been any specific guidance as such, on the tax treatment of OTA commissions. Any business which has thus far been subject to a WHT audit by the MIRA is well aware that the MIRA has not taken up the issue of ‘deemed commission’ in their past tax audits.

However, MIRA issued a circular on 28 December 2016, which, in simple terms, states that regardless of the payment arrangement, OTA commissions would be subject to WHT (and this circular was applicable from 1 January 2017). Although it has not issued any circular or guidance on the GST treatment on OTA commissions, you might have noticed that in the MIRA’s recent audits, they have started charging GST on the deemed commission as well.

What can you expect?

Following the MIRA’s new approach in the tax treatment of OTA commissions, regardless of the model practised between you and the OTA, you are now required to:

- Charge GST on the ‘Sell Rate’ offered by the OTA

- Charge WHT on the ‘deemed commission’ charged by the OTA

You can expect MIRA to charge WHT on the deemed commission from all OTA transactions (example: Agoda, Expedia, etc) that arose after 1 January 2017.

In case of GST, there is no cut-off date as such. However, we have observed that in its most recent audits, the MIRA has charged GST on the ‘deemed commission’ amount which extends to the whole audited period. That being the case, if you have recently been selected for a GST or WHT audit, or if there is an ongoing audit by the MIRA, the MIRA, will most likely charge additional GST and WHT on these transactions, if you haven’t declared them already.

How do you calculate the ‘deemed commission’?

The problem with the Merchant Model is that for management accounting purposes, most businesses only recognize the ‘net revenue’ as their revenue (as they do not want to inflate revenue, for obvious reasons). Further, since the OTA is not raising an invoice to you with the commission amount, you will find it quite difficult on ascertaining the correct amount to pay WHT on this transaction.

An alternative approach, in accounting for GST and WHT, is to manually calculate the amounts subject to tax, as illustrated in the below example.

Assume that Mark’s booking to stay at Amazing Resort was made with Expedia, under the Merchant Model. Under the agreement with Expedia, the resort has agreed to a “compensation percentage” of 20%. Below is the rate breakdown:

| Details |

Amount |

Hotel’s share (80%) |

Expedia’s share |

| Price |

576.00 |

460.80 |

115.20 |

| 10% Service Charge |

57.60 |

46.08 |

11.52 |

| 12% GST |

76.03 |

60.83 |

15.21 |

| NETT |

709.63 |

567.71 |

141.93 |

| Green Tax |

12.00 |

12.00 |

|

| Amount inclusive of taxes |

721.63 |

579.71 |

141.93 |

Note: In the above example, you can see that Expedia pays the Hotel the full amount of GRT, while GST and service charge is apportioned based on the commission percentage (and I understand this is a common practice with some OTAs). In accounting for the correct amount of tax, it is important to identify how these taxes collected by OTA are remitted to the Hotel.

Upon check-out, the resort invoices Expedia for its share of revenue including GST which adds up to USD 579.71. The GST amount paid to MIRA by the resort is as below:

| Description |

Label |

Formula |

Amount |

| Total revenue including taxes |

A |

579.71 |

|

| GRT |

B |

12 |

|

| GST |

C |

(A-B)/112*12 |

60.83 |

However, following the MIRA’s new approach, GST must be paid on the ‘full value of supply’ which can be calculated as follows:

| Description |

Label |

Formula |

Amount |

| Resort’s share of revenue |

A |

579.71 |

|

| GRT |

B |

12 |

|

| Expedia Compensation % |

C |

20 |

|

| Expedia Compensation amount |

D |

((A-B)/(100-C)*C) |

141.93 |

| Additional GST payable |

E |

D/112*12 |

15.21 |

When you calculate additional GST as per this method, effectively you end up paying GST on the OTA’s Published price which is shown below:

| Description |

Label |

Formula |

Amount |

| Total Published Price |

A |

721.63 |

|

| GRT |

B |

12 |

|

| Total GST on the published price |

C |

(A-B)/112*12 |

76.03 |

| GST paid to MIRA |

D |

(60.83+15.21) |

76.03 |

Withholding tax on the compensation amount is calculated as follows:

| Description |

Label |

Formula |

Amount |

| Expedia Compensation amount |

A |

141.93 |

|

| Gross amount |

B |

B/0.9 |

157.7 |

| WHT @10% |

C |

B x 0.1 |

15.77 |

There are certain challenges when applying this calculation. For one thing, you have to keep record of the rate of compensation/commission charged by the OTA for each individual booking so that the correct amount of tax can be calculated. Further, you must also consider this change in deciding the rate offered to OTAs as you most likely, have to suffer the additional GST arising from these transactions.